Modern global capital markets are operating amid a profound divide between technological triumph and growing macroeconomic instability. Large institutional investors are forced to simultaneously weigh the unprecedented commercial potential of generative AI and sudden escalations in military conflicts, turning daily trading activity into a complex balancing act. We at FinancialMediaGuide note that this duality is creating an entirely new investment reality in which fundamentally strong corporate performance must compete with geopolitical shocks for market liquidity.

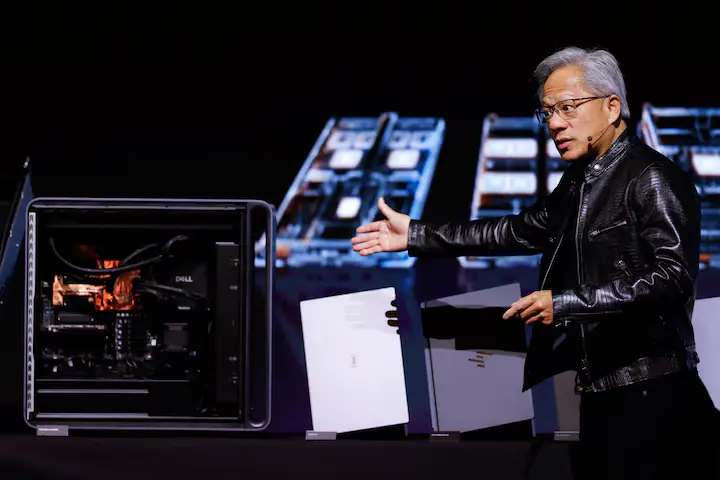

At the center of the current market landscape remain the statements of senior executives at semiconductor giant Nvidia, whose shares are widely regarded as the primary barometer of the AI industry’s health. Speaking on Tuesday at a major industry conference in Taipei before electronics and hardware manufacturers, CEO Jensen Huang confirmed that the sector continues to operate under conditions of acute supply constraints. The remarks came just one day after Nvidia’s market valuation stabilized at $5 trillion, supported by the unveiling of a new chip architecture designed to compete directly with offerings from AMD and Intel. According to Huang, the company’s technological foundation provides ample resources for highly sustainable long-term growth, but manufacturing capacity still lags far behind market demand. Independent research further confirms that the key bottleneck remains the critical shortage of advanced CoWoS chip packaging capacity, a constraint expected to persist at least through the end of the year. We at FinancialMediaGuide view this as clear evidence that the physical limits of silicon infrastructure have become a major obstacle to global digitalization, directly influencing capital flows across the world’s largest technology conglomerates.

Under stable macroeconomic conditions, news of such massive unmet demand would likely have triggered a broad rally in the shares of Asian high-tech component suppliers. However, trading across the Asia-Pacific region ended on a volatile note due to escalating tensions in the Middle East. Investors adopted a cautious stance amid concerns over the potential collapse of the fragile ceasefire between the United States and Iran. As a result, the broad MSCI Asia Pacific ex-Japan Index declined by 0.1%, while U.S. S&P 500 E-mini futures fell 0.4%. According to analysts at FinancialMediaGuide, this performance reflects a classic flight-to-safety dynamic in which regional geopolitical shocks temporarily outweigh positive corporate developments.

The commodities sector faced similar pressure, with Brent crude oil prices declining 0.7% to $94.30 per barrel. The pullback partially offset the previous rally that had been fueled by official threats from Tehran to completely suspend diplomatic contacts with Washington. Additional uncertainty emerged from the Levant, where Lebanon’s announcement of a partial ceasefire between Israeli forces and Hezbollah initially offered markets hope for de-escalation. However, subsequent reports from the Israeli military regarding the interception of two incoming projectiles quickly restored a geopolitical risk premium across financial markets.

The most dramatic price swings were recorded in South Korea. The Kospi Index plunged 3.3% after surging 1.7% earlier in the session, when it reached a new intraday record high. Stock exchanges in Hong Kong and mainland China helped prevent a deeper regional decline, stabilizing amid targeted interventions by Chinese state-backed funds. Meanwhile, European markets opened modestly higher, with pan-European equity futures gaining 0.4%, Germany’s DAX advancing 0.3%, and the UK’s FTSE rising 0.1%.

European traders are positioning ahead of quarterly earnings reports from technology leader Palo Alto Networks and retailer Dollar General, while also assessing fresh macroeconomic data from France. April figures showed a widening budget deficit, which expanded to €69.6 billion due to declining tax revenues amid the broader slowdown in the Eurozone economy and rising debt-servicing costs. We at FinancialMediaGuide emphasize that deteriorating fiscal conditions among Europe’s leading economies place significant constraints on future stimulus programs, forcing investors to demand higher yields on European sovereign bonds.

At the same time, the U.S. legal system has established a precedent that could significantly reshape the landscape for short selling. A U.S. jury found prominent investor Andrew Left guilty of securities fraud in a case brought by the Department of Justice. The verdict represents a major setback for short sellers, many of whom have spent years using public reports alleging corporate misconduct to profit from declining share prices. Left’s sentencing is scheduled for August 31. We believe this precedent may substantially reduce speculative pressure on public companies and contribute to a healthier market environment, as regulators have clearly defined the boundaries of acceptable conduct in public campaigns against businesses.

At Financial Media Guide, we expect global financial markets to remain highly fragmented and volatile through the remainder of the current financial half-year. Structural shortages of semiconductor products will continue to provide fundamental support for chipmakers’ valuations and sustain elevated sector multiples. However, the overall direction of equity indices will remain closely tied to developments in Middle Eastern negotiations and the pace of fiscal normalization across the Eurozone.

Based on our analysis, we recommend that investors shift their focus toward manufacturers of lithography equipment and cooling systems for data centers, both of which stand to benefit from ongoing capacity expansion regardless of end-device demand conditions. We also recommend temporarily increasing allocations to short-term U.S. Treasury bills to reduce portfolio risk during periods of heightened market volatility.